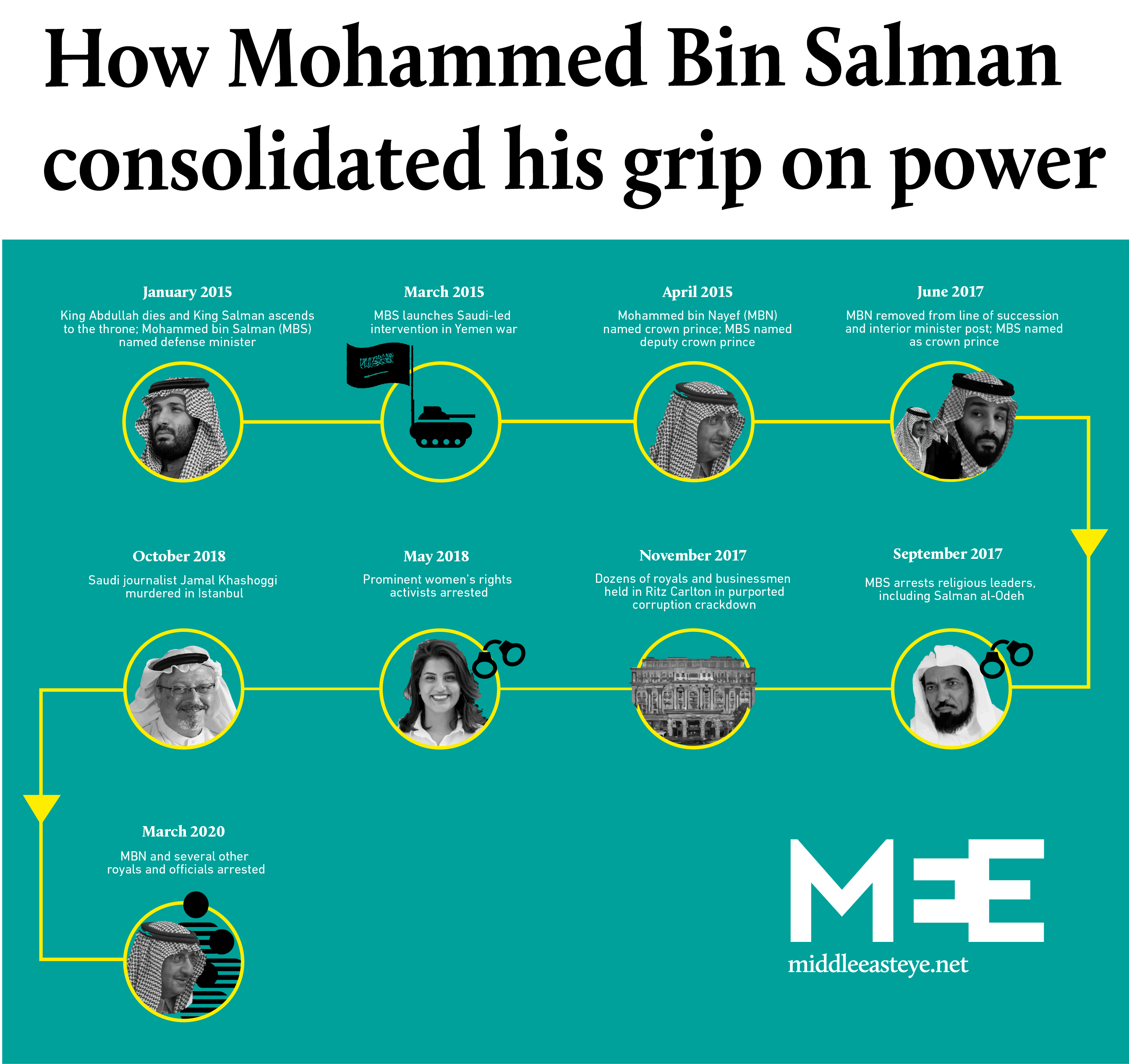

For much of its existence, Saudi Arabia was stable.

It was an absolute monarchy which dealt with dissidents ruthlessly. Arbitrary detention, torture, disappearanc es at home and kidnappings abroad were its staple diet. Wahhabism was used as a brutal method of religious and social control. Kings bought popularity by handouts such as paying for degrees abroad. This is how the kingdom functioned – for decades – with relatively few internal problems.

es at home and kidnappings abroad were its staple diet. Wahhabism was used as a brutal method of religious and social control. Kings bought popularity by handouts such as paying for degrees abroad. This is how the kingdom functioned – for decades – with relatively few internal problems.

It was ruled by a council of princes, sons of its founder King Abdulaziz, who shared the goodies out among themselves, ensuring that each branch was represented: the Nayefs got the interior ministry, the Sultans the defence ministry, the Abdullahs the National Guard, the Faisals the foreign ministry and the Talals the media, and so on.

Lucrative ministerial portfolios were handed down from father to son like the family silver and in that way expertise and experience were accrued and kept within the family.

Fierce rivalries

When crises struck, collective decisions were taken. A family council was convened and decisions were taken slowly and with great, almost excessive, caution. Saudi foreign policy, it was said, was conducted behind bead curtains, it was that inscrutable. The kingdom was wholly in the service of US military and oil interests in the Gulf, but within that large rubric, it had its own agendas.

For all the Saudi internal clan tensions, there was stability

There were succession disputes to compare with what happened this week, such as when Crown Prince Faisal challenged the authority of King Saud in the 1960s. But these were swiftly and quietly resolved. When Saud lost that power struggle and was forced to fly off into exile, he was waved goodbye at the airport by his ouster.

There were also fierce rivalries. The murdered Saudi journalist Jamal Khashoggi was a supporter of Mohammed bin Nayef who ruled the interior ministry with an iron fist, imprisoning and executing hundreds, but the same could not be said of Prince Ahmed bin Abdulaziz, who released prisoners when he took over the same post.

Khashoggi never tired of saying that there was no difference between Prince Ahmed and his nephew Mohammed bin Nayef, save that one was crown prince and the other not. I remember thinking this was overly harsh.

But for all the internal clan tensions, there was stability.

No more. This period has passed. Look at how violently the Saudi royal yacht has been rocking and this list is the work of just the last few days.

Hasty decisions

A purge has been launched against a brother of the king and son of the founder Abdulaziz, considered, until now, untouchable; the Houthis overran cities in the Khub Walshaaf district on the border with Saudi Arabia, before being pushed back on Monday; the borders of the country have been closed, Umrah pilgrimage to Mecca stopped only six weeks before the start of Ramadan and the Eastern Province closed down, while only a handful of coronavirus infections have been officially reported; a three-year-old agreement with Russia broke down, and Riyadh flooded the world market with oil, sending the price plunging at levels not seen since the 1991 Gulf War.

Mohammed bin Salman deals with one catastrophe by moving on to the next

Each event is down to one man: Mohammed bin Salman. He deals with one catastrophe by moving on to the next. Decisions are taken with the speed of a rapid fire machine gun, without a second’s thought about the consequences.

Take the oil decision. The Financial Times calculated the decision would punch a $140bn hole in the revenue this year of the six Gulf states if the price of crude remained at $30 a barrel. The rich Gulf states Kuwait, UAE and Qatar can cope, but Saudi Arabia, Bahrain and Oman cannot. Saudi Arabia’s budget needs $83 a barrel to break even.

Maybe this was why one of the architects of the 2030 economic reform plan, Mohammed Tuwaijri, was removed from the Ministry of Economy and Planning last week and pushed upstairs as an advisor. This was the man who warned that if Saudi Arabia did not reform its finances, it would be broke in “three to four years”.

That was over three years ago.

The gambler

At best, pumping out oil at the rate it is doing should be classed as a gamble. But this is only one of a growing list. The next gamble is trashing Saudi Arabia’s carefully fabricated image as a leader of the Sunni Muslim world and the reliable custodian of the Muslim holy shrines.

This was a mighty source of Saudi soft power. It was also a source of legitimacy for the House of Saud.

The Bayaa, or Allegiance Council, was created in 2007 by King Abdullah to secure the future succession to the Saudi throne. Previously this had been the sole prerogative of the king.

Its main purpose was to avoid a power struggle and ensure a smooth succession after all of the sons of Abdulaziz, the founder and first king of Saudi Arabia, had died.

The council is intended to ensure the collective loyalty to the monarch of all of the branches of the Saudi royal family. It was originally composed of 34 members, representing the number of sons of Abdulaziz who themselves had male offspring. When a member died or resigned they were replaced by their son, or a place was allotted to their branch of the family in the future.

The council has two principal roles: to determine if the king is capable of fulfilling his functions or to accept the king’s resignation; and to announce who the new crown prince will be following the accession of a new king, chosen nominally from three candidates offered by the king.

While the choice of crown prince is determined by a vote, in reality the council is expected to execute the new king’s wishes.

However, a small but important clause in the council’s rules is that if the king is one of the founder’s grandsons, his crown prince cannot be from the same branch of the family (such as a brother or son).

This means that if Mohammed bin Salman becomes king, he would be expected to choose one of his cousins as crown prince.

When the then prime minister of Malaysia, Mahathir Mohamad, invited the leaders of Turkey, Qatar and Iran, all Saudi Arabia’s rivals, for a mini-summit of Islamic leaders in Kuala Lumpur last December, Mohammed bin Salman saw red.

Instead of embracing the summit, he turned his social media goons onto it, creating in the process a rival to the Organisation of Islamic Co-operation. He bullied Pakistan’s Prime Minister Imran Khan into not attending. Khan later apologised to Mahathir.

The result? The standing of Malaysia, Turkey, Qatar and even Pakistan have risen in the Sunni Islamic world and Saudi Arabia’s has diminished. But not as quickly as it is doing with its decision to close its borders to Umrah pilgrims, six weeks before the start of Ramadan.

The corona blackout

The spread of the coronavirus in the kingdom is not known, because doctors are not testing for the virus, and like Egypt, efforts are made to underplay its existence. Does anyone seriously believe that at a time when there are 9000 cases in Iran, 189 cases in Bahrain, 71 cases in Iraq, 74 cases in the UAE, 58 cases in Kuwait, there are only 21 cases in Saudi?

Nor is it known how long these closures will last. The resentment these arbitrary edicts are creating inside the kingdom and outside it is growing and will quickly become threatening to the crown prince. He is losing a lot of income but he is also gambling with his religious legitimacy as Saudi Arabia’s next king.

So the Saudis are stuck. They dare not admit the scale of the problem, but neither can they justify on medical grounds the decision to close the Eastern Province. There are, however, political motives to quarantine the Shia majority areas of Qatif and Al Ahsa.

Which leads me to Mohammed bin Salman’s latest decision to arrest his uncle Ahmed bin Abdulaziz.

The Trump cover

He knew, because Ahmed let this be known before he left his home in London, that his uncle got assurances from MI6 and the CIA that he would not be arrested on his return. By defying this injunction, the Saudi crown prince is relying on the cover given to him by US President Donald Trump and his son-in-law Jared Kushner.

Supposing however that neither of these two men are in office after November. What does Mohammed bin Salman think would happen to the voluminous CIA files on him? They would be passed to – say – a President Joe Biden, a declared Zionist with Israeli support, but who might be expected to have a very different view of bin Salman personally.

Anyone expecting Biden to change US foreign policy in the Middle East is in for a long wait, but that does not mean nothing would change.

Biden would have a personal interest in unravelling Trump’s private network of foreign allies. Mohammed bin Salman is one of them. The US, however, would remain a backer of the kingdom but not necessarily the new king, even if bin Salman presents the incoming president with a fait accompli.

At the very least, eliminating known CIA assets in the kingdom, like Mohammed bin Nayef, relies on the assumption that there will always be someone in the White House to suppress the instincts of the agency to fight back. In the current volatile political climate in the US, that is a huge gamble.

Would anyone – bar Trump – want a crown prince this unstable to become king in a country which, unlike Russia, China and Iran and Turkey, is a US military protectorate?

This is the biggest gamble Mohammed bin Salman has taken in his short career as crown prince. The real problem is that bin Salman, and his advisors, may be too stupid to realise the mistake he has just made.

The views expressed in this article belong to the author and do not necessarily reflect the editorial policy of Middle East Eye.

ARTICLE TWO

Oil price turmoil: How Saudi Arabia’s $100bn gambit could backfire

In 1985, US Vice President George HW Bush visited Saudi Arabia to pressure the kingdom to flood the global market with cheap oil and squeeze the energy revenues of the Soviet Union.

The move pushed oil below $10 a barrel, reasserted Saudi Arabia’s dominance as the world’s top oil player, and dealt what some consider a crippling below to the ailing Cold War superpower.

‘Saudi Arabia has offered deep discounts to East Asia, and also to Europe to undercut Russian exports. This is a bold gambit’

– Justin Dargin, Oxford University

Fast forward to March 2020, and an oil price war is being played once again, with consequences for Washington, Moscow and the entire global economy.

Recent production cuts agreed between OPEC+ members, the global oil cartel, fell apart as Saudi Arabia clashed with Russia over prices and Riyadh upped production to 13 million barrels per day (bpd). The oil price dropped by 25 percent to $36 a barrel on Monday.

The move is considered a gambit by both Saudi Arabia and Russia, which did not want as deep a price cut as Riyadh, to counter the growing market share of the US shale industry.

“From the Russian point of view they are seeking a redistribution of market share, which is the same thing the Saudis want. This dance between the two is like a relationship between a separated couple; they are arguing over relationship dynamics and will soon recognise the market has adjusted to where they can sit down and clink glasses,” said Theodore Karasik, a senior advisor to Gulf State Analytics, a Washington-based consultancy.

Such a pricing tactic was tried in 2014, when OPEC upped production to bring prices well below $100 a barrel to muscle out the US shale sector, which required much higher extraction costs, at around $60 a barrel, to be competitive compared to conventional oil producers.

Saudi Arabia can pump a barrel of oil from certain fields for as low as a $1.

While many US shale businesses went bust and operations stalled, the move backfired.

“Operations became consolidated and more efficient, and the break-even price dropped. In a nutshell, the US shale industry actually became stronger and leaner, and is now better placed than it was 2014, able to sustain prices of around $30 a barrel for a bit of time,” said Justin Dargin, an energy expert at Oxford University.

“You can’t put the genie back in the bottle, and that is a misreading they [Moscow and Riyadh] should have learned from 2014,” he added.

Mortgaging the future

Before the 2014 price drop, the Gulf countries had amassed huge revenues when oil was over $100 a barrel. The National Bank of Kuwait (NBK) estimated in 2011 that for every $1 increase in a barrel of oil, GCC states accrued an additional $4.5bn a year in revenues.

But in the years since, with lower oil prices, GCC countries used such surpluses to keep their economies afloat and fund diversification strategies to wean their income generation off oil, such as the Vision 2030 programmes promoted by Saudi Arabia, Qatar and Abu Dhabi.

‘Since the last oil price cut, the GCC has burned through foreign reserves, but they rode it out. The discussion now is that they can’t do it this time’

– Guy Burton, adjunct professor at Vesalius College

“Since the last oil price cut, the GCC has burned through foreign reserves, but they rode it out. The discussion now is that they can’t do it this time,” said Guy Burton, adjunct professor at Vesalius College in Brussels, and a former assistant professor at the Mohammed Bin Rashid School of Government in Dubai.

The GCC’s finances have become so perilous that the IMF warned in a February report that “the region’s aggregate net financial wealth, estimated at $2 trillion at present, would turn negative by 2034 as the region becomes a net borrower”.

With oil prices at $100 a barrel, wealth would be exhausted by 2052, “while a real oil price of $20 a barrel would bring it forward to 2027.”

Riyadh’s price cut move could therefore speed up such a decline in revenues to within this decade, with a fiscal deficit of more than $100bn possible this year.

“If the price is low for an extended period it will put Vision 2030 at significant risk. They need to create six million jobs for the Saudi youth, and it was intended for much of that to be taken care of by the private sector,” said Dargin.

Saudi Arabia’s economy was already struggling, growing by just 0.3 percent last year, while the construction sector has dropped by 25 percent since 2017. Infrastructure projects have stalled, with investment nearly half in recent years from a peak of $40 billion in 2014, according to regional projects tracker MEED Projects.

The kingdom’s GDP per capita has also declined, from $25,243 in 2012 to $23,338 in 2018, according to the World Bank.

“There is a need to rethink these Vision 2030s, and revise them. COVID-19 has also destroyed plans,” said Burton, with Riyadh having cancelled Umrah this year, and Dubai’s 2020 World Expo in doubt.

The annual Hajj and Umrah pilgrimages are major contributors to Saudi Arabia’s economy, attracting close to 10 million pilgrims per year and generating over $8bn in revenues, while the kingdom planned to attract 30 million pilgrims a year for Umrah under Vision 2030.

Given such blows to its economic prospects, “a lot of people looking at the [Saudi price cut] issue are saying, ‘What are you doing? You are mortgaging your future,’” said Karasik.

But it is not only Saudi Arabia that will feel the pinch of lower oil prices.

Karasik said that while the Saudi price cut was aimed at bringing pressure on US shale, it had a secondary regional goal. “In a political sense, it is putting pressure on particular states to become subservient to those that have the cash.

“If oil is way below levels to balance state budgets in the Middle East, this is going to become a negotiating tool between stronger and weaker Arab states.”

Pressure on Iran and Iraq

Iraq and Iran, both outside of Riyadh’s political influence, will be particularly impacted, with a $10 drop in oil prices reducing conflict-riven Iraq’s current account by $14bn, according to Institute of International Finance (IIF) calculations.

The result for Iran will be just as dire. “Iran is under renewed American sanctions, is a COVID-19 world hot spot, there were protests in the streets not too long ago and now, with oil around $30 a barrel, I don’t know how Iran will be able to survive. It definitely doesn’t look good for them,” said Dargin.

Tehran has appealed to the International Monetary Fund (IMF), for the first time since the early 1960s, for a $5bn assistance package to deal with the crisis. Iran has the world’s highest fiscal break-even oil price – the price needed per barrel to balance the budget – at $194.6, while Saudi Arabia needs $85.7, the UAE $64.7 and Russia $42.

While Saudi Arabia’s finances are not overly rosy, it can ride out lower prices to achieve its more immediate goals.

“We have to bear in mind that the economy’s balance sheet is very strong, and has large amounts of government savings. While it will be running quite a large deficit, at 15 percent of GDP, that is not as bad as it was five years ago, and if oil prices recover then it will be smaller,” said William Jackson, chief emerging markets economist at Capital Economics, a macroeconomic research firm in London.

The firm noted that oil production in Saudi Arabia, the UAE and Kuwait “would remain profitable even if oil fell to as low as $15 per barrel”.

Saudi-East Asia ties

Burton said that as Saudi Arabia and other GCC states have been diversifying foreign investments, particularly to East Asia, the main buyer of Gulf crude, there is largess to weather a drop in oil prices.

“There is a deepening of economic relations, and it is both ways, between the Gulf and Asia. You can see they are hedging their bets,” said Burton.

‘Anything can happen at this moment, with multiple black swans events, and we don’t know how COVID-19 will impact oil production’

– Justin Dargin, Oxford University

Saudi Arabia has also invested heavily in refineries in Asia to secure a long-term market share. The kingdom is South Korea’s single largest oil supplier and has a stake in around half of the country’s refinery capabilities, noted Karasik.

“Saudi Arabia has offered deep discounts [in oil] to East Asia, and also to Europe to undercut Russian exports. This is a bold gambit,” said Dargin.

A further aspect of Riyadh’s decision to bolster output is to lay the groundwork for new oil field developments slated to come online in the next few years, as well as in the UAE, a key ally of Riyadh.

Lower oil prices would allow these Gulf states to bring such new capacity onto the market, which would be hindered if they had to abide by the same production cuts under OPEC+ agreements.

“A different type of energy market is emerging because of announcements of new discoveries of oil and gas in Saudi Arabia and the UAE. These need to be calculated into future demand and supply,” said Karasik.

Calculating such future demand seems increasingly fraught, with the oil price now in lock-step with COVID-19, which has caused stock markets to drop, transportation to be interrupted, and propelled a deeper economic recession in the Middle East and much of the world.

Before the oil price cut, demand for oil was expected to decline by 0.3 million bpd in 2020, according to the IIF, compared with growth of 1 million bpd predicted at the beginning of the year.

“Anything can happen at this moment, with multiple black swans events, and we don’t know how COVID-19 will impact oil production – will oil workers even be able to get to work?” said Dargin.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/thenational/WC6UPQPLY5ECVKFOCP6WHWV3XU.jpg "UK: How rising cost of living is changing Muslim consumers in the UK")